The Hightower Report Wednesday July 21, 2021 14:04

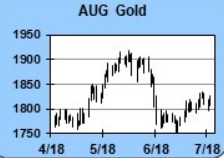

GOLD / SILVER We continue to think gold and silver lack a definitive fundamental focus, but we think the charts favor the bear camp to start today. The markets came under pressure yesterday due to a significant washout in equities and from fears of a return to lockdowns. Those fears were given added credence by the overnight health warning from the WHO. Furthermore, the markets failed to recover despite a 600-point rally in the Dow yesterday, in a sign that “risk on” and “risk off” are not a primary concern for precious metal prices. The Dollar Index remains in a bullish technical track, with a new high for the move forged again overnight and many traders projecting further gains. The Index has reached its highest level since early November. The lift from declining interest rates has been more than countervailed by strength in the dollar and fears of slowing. While the gold market has not paid significant attention to the supply-side of the equation, 4 of 5 gold mining companies reporting production overnight showed increases, while a Russian firm indicated its 2021 first-half production declined by 39%. In a story that could be considered supply or demand orientated, the IMF released statistics overnight of central bank gold for June and it showed increases in Brazil, Czech Republic, Uzbekistan, India, UAE, and Serbia and reductions in Turkey and the Philippines. Gold ETF holdings posted a decline of 59,131 ounces yesterday, leaving the year-to-date change down 6.4%. Going forward, we see more vulnerability than opportunity on the long side, and we also remain concerned about where US daily infections are headed. It could be very difficult to see a sudden setback in daily infection tallies, especially given that the Delta variant is highly contagious. With the silver market forging a fresh lower low for the move and violating the $25.00 level again, the charts favor the bear camp. However, the September silver contract also aggressively rejected last night’s probe below $25.00 which was the second day in a row for that type of action, and ETFs saw a large inflow yesterday of 7.1 million ounces, an increase of almost 1%. All roads seem to point down, with the bear camp seeing the inflation story line deflated by the prospect of renewed virus headwinds.

PGM

In a slightly bullish technical development, the September palladium contract has forged a 3-day high overnight, but investors remain cool toward the market, with ETF holdings yesterday increasing by a mere 947 ounces. However, they are 9% higher on the year, and the market is relatively small, so a moderate increase in investments should be a cushion to prices.

The PGM markets forged significant divergence yesterday, with palladium regaining a portion of the large losses forged on Monday and in turn forging a double low around $2,565.50.

The PGM markets should have drafted support from news that Russia’s Nornickel saw its second quarter palladium production decline 28% from the first quarter. Apparently, the company saw accidents and other operations delays that resulted in the lost output. For the palladium market to post consistent gains ahead probably requires a return to global risk-on psychology or some favorable economic news from China. A normal retracement of the significant July washout allows for a bounce up to $2,686.80 without disrupting the mid-July downtrend pattern. Unfortunately for the bull camp in platinum, the market was unable to benefit from gains in gold and palladium and was also unable to benefit from a sharp recovery in equities yesterday. The market did not seem to benefit from news that Russian Nornickel showed a 27% decline production in the second quarter, but that news was heavily countervailed by reports that Anglo-American production increased. It should be noted that platinum ETF holdings yesterday increased 6,391 ounces, bringing the annual gain to +2.9%. In the meantime, $1,050 level is initial support, with fresh long positions likely needing to locate stops below $1,030.

MARKET IDEAS: We favor the bear camp, as gold and silver have been inconsistent with their reactions to fundamental stories and have showed consistent divergence in prices. In other words, the bull camp lacks a clear theme to propel prices higher, while a deflationary concern is drifting back into the market because of the resurgence of infections. A key pivot point in August gold is seen today at $1,802.90. Pushed into the market, we would be sellers on rallies above $1,825.

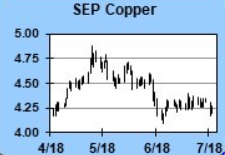

COPPER

Better global sentiment & short covering buy China news limits

We are surprised to see September copper up on the day in the wake of news that the Chinese government will auction 30,000 tonnes of the metal next Thursday. Apparently, the government is threatening speculators they think are responsible for high material costs. If equities resume their aggressive declines, it could throw September copper right back down to the $4.20 level. The market once again rejected a sub-$4.20 trade yesterday, and equities have recovered today, but the 14-cent washout in prices and emerging fears of deflation give the bear camp some confidence. While not a significant negative development, Anglo-American quarterly copper production increased 2%, but that news was countervailed by a 11% drop in Nornickel production (10,000 tonnes) for the second quarter. Another development in favor of the bull camp overnight was a prediction by Goldman Sachs that commodities were poised for another wave higher after the recent washout. The market was partially deflated by mixed US housing starts and permits data yesterday, and it is logical to assume that prices will remain vulnerable to further increases in US infection numbers.

MARKET IDEAS: We see the positive early action in copper prices as impressive, especially given the announcement by the Chinese government to sell more copper reserves next week. Maintaining a positive global equity market psychology is critical for the bull camp if they are to extend the current bounce to the middle of the last 40 days’ consolidation. While we think that the September copper contract will generally respect $4.25, we will not discount the potential to see periodic tests of lower support levels at $4.2030, $4.1945, and at this week’s low of $4.1665.